Risks

Risks

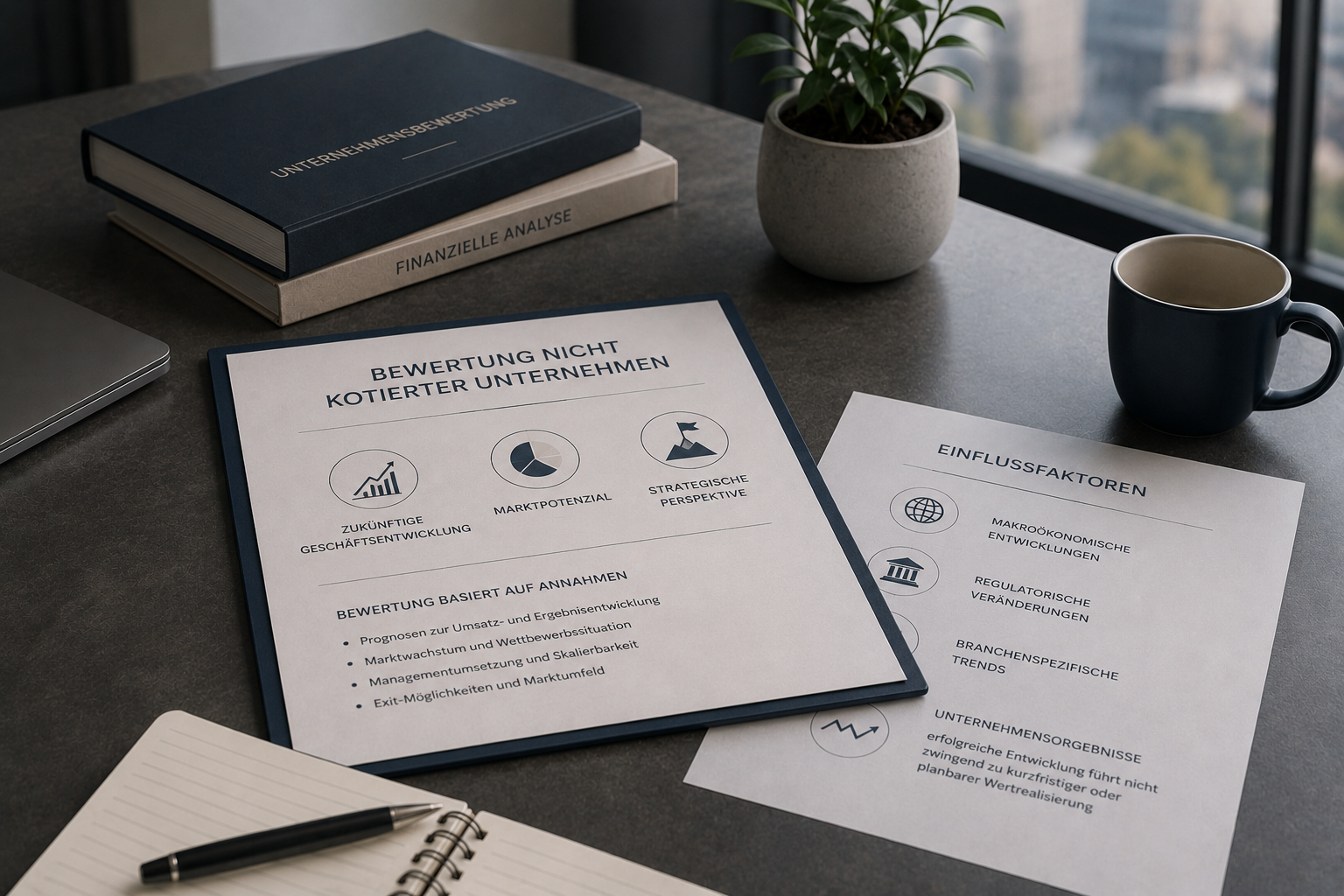

Key characteristics of private equity investments

Private equity investments differ fundamentally from exchange-traded assets. They are equity investments in non-listed companies, where the development of value depends primarily on the operating performance of the business. Because there is no organised market liquidity, no continuous market price exists and the shares cannot be traded at any time.

These structural features mean that private investments carry specific risks which investors should understand and assess carefully.

Principles for a sound investment decision

An investment decision should never be made under time pressure. Take the time needed for careful review and, where appropriate, consult external experts or seek an independent second opinion. In the private equity market, any urgency or push for a quick decision should always be treated with caution.

Private equity investments are entrepreneurial risk investments. No private equity investment can credibly be described as safe. The worst case is the complete loss of the invested capital. Promises of profit or guaranteed returns without an adequate presentation of the risks should be regarded as a warning sign.

Since 1 January 2020, financial services in connection with the placement of capital have been governed by the Swiss Financial Services Act (FinSA, in German: FIDLEG). Among other things, this law sets out information duties, conduct rules and the registration of client advisers. Investors should make sure that the applicable regulatory requirements are observed and that the relevant information can be provided in a clear and traceable form.

Information that is relevant to the decision should always be documented and reflected in the contractual basis. Verbal commitments or non-binding statements cannot substitute for written documentation. The official documents of the company and the contractual agreements are decisive.

The business case presented, meaning the business model and its economic plausibility, forms the central basis for the decision. A thorough review of the market environment, competitive position, management capability and capital structure is essential.

Investors should also form a personal impression of their counterpart. Open dialogue, willingness to address critical questions and the opportunity to get to know the company and its leadership are hallmarks of a credible investment process.

In addition, investors should verify that the adviser they are dealing with is properly registered in a recognised register of client advisers, as required by applicable regulation. Registration is conditional on demonstrating the relevant expertise.

Business risk and the risk of total loss

Private equity is entrepreneurial risk capital. Investors provide equity capital and share in the economic success of a company. At the same time, they bear the full business risk.

Companies may fail to meet their strategic objectives, products may not gain traction in the market, regulatory approvals may not be granted, or market conditions may develop unfavourably. In such cases, the value of the company can decline significantly.

The worst case in any private equity investment is the complete loss of the invested capital. Private equity investments are therefore not comparable to conservative forms of investment.

Liquidity and timing risks

Investments in non-listed companies are generally long-term in nature. A regulated secondary market typically does not exist, and investors have no general entitlement to an early exit.

The holding period can extend over several years and depends on how the company develops as well as on market conditions. A planned exit may be delayed or may have to take place under unfavourable conditions.

Investors should therefore only commit capital they can afford to set aside for an extended period.

Funding and dilution risks

Growth companies may need additional capital over the course of their development. Further funding rounds can lead to dilution of existing investments if investors do not participate proportionally.

Financing conditions can also change, for example through rising interest rates, restricted access to capital or shifts in market sentiment. Such factors can affect the valuation of a company and the strategic options available to it.

In certain situations, additional capital may be required to secure the continuation of the business.

Market and valuation risks

The valuation of non-listed companies is based on assumptions regarding future business development, market potential and strategic outlook. These assumptions may prove not to hold.

Macroeconomic developments, regulatory changes or sector-specific trends can affect the economic situation of a company. Even successful operational progress does not necessarily lead to a short-term or predictable realisation of value.

Investor responsibility

Any investment decision in the private equity space should rest on an independent and careful review. Investors should form a comprehensive picture of the business model, the market environment and the underlying structure of the investment.

Nordstein places great importance on presenting the relevant information transparently and within the framework of regulatory requirements. The decision to invest, however, rests solely with the investor.